1. Asia Pacific Plant Protein Market Overview - Definition, scope, and significance?

The Asia Pacific Plant Protein Market encompasses the production, processing, and distribution of protein derived from plant sources such as soy, wheat, and pea. It includes isolates, concentrates, and protein flour used across food and beverage applications, including protein beverages, dairy alternatives, meat alternatives, protein bars, and bakery products. The scope extends from raw material sourcing to final consumer-ready products, covering both industrial manufacturers and foodservice providers. Significance lies in the region’s growing population, rising health consciousness, and increasing demand for sustainable, animal‑free protein, positioning plant protein as a critical component of future food security and nutrition strategies.

2. Asia Pacific Plant Protein Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising consumer awareness of health benefits, governmental support for plant‑based diets, and the need to reduce greenhouse‑gas emissions associated with livestock production. Urbanization and higher disposable incomes further fuel demand for convenient, protein‑rich products. Restraints stem from entrenched cultural preferences for animal protein, price sensitivity, and regulatory variations across countries. Challenges involve ensuring consistent raw‑material quality, scaling up processing capacity, and managing allergen concerns. Opportunities arise from product innovation (e.g., hybrid proteins), expansion into emerging markets such as Vietnam and the Philippines, and collaborations between ingredient suppliers and food manufacturers to create fortified, clean‑label offerings.

3. Asia Pacific Plant Protein Market Growth Trends - Current and emerging trends shaping the market?

Current trends highlight a shift from simple protein supplements to functional foods that combine plant protein with vitamins, probiotics, or adaptogens. Manufacturers are increasingly offering pea‑protein isolates as a hypoallergenic alternative to soy. The “flexitarian” movement is driving blended protein products that mix animal and plant sources to ease transition. Digital commerce and direct‑to‑consumer channels are accelerating product launches, while sustainability certifications are becoming a purchasing criterion. Emerging trends include the use of AI for formulation optimization and the exploration of novel sources such as lentil or chickpea protein to diversify the supply base.

4. COVID-19 Impact on the Asia Pacific Plant Protein Market - Pandemic effects and recovery trajectory?

The pandemic initially disrupted supply chains for raw legumes and soybeans, leading to short‑term price volatility. Simultaneously, lockdowns boosted home cooking and an increased focus on immunity‑supporting nutrition, driving demand for plant‑protein powders and ready‑to‑drink beverages. Post‑2020, the market experienced a rapid recovery, with consumer habits retaining a stronger preference for shelf‑stable, high‑protein products. The recovery trajectory is positive, supported by continued e‑commerce growth and a resilient shift toward health‑centric purchasing that is expected to sustain the market’s upward momentum.

5. Asia Pacific Plant Protein Market Competitive Landscape - Major competitors and market consolidation?

The competitive environment is characterized by a mix of global agribusiness giants and specialized protein innovators. Key players such as Archer Daniels Midland Company, Cargill, and Koninklijke DSM N.V. dominate the bulk raw‑material segment, leveraging extensive sourcing networks. Specialty firms like Axiom Foods, Inc., Kerry Group, and Roquette Fr focus on high‑purity isolates and customized solutions. Recent consolidation activities include strategic acquisitions of smaller pea‑protein firms by larger corporations to broaden their source portfolio and accelerate R&D capabilities, reinforcing a trend toward vertical integration.

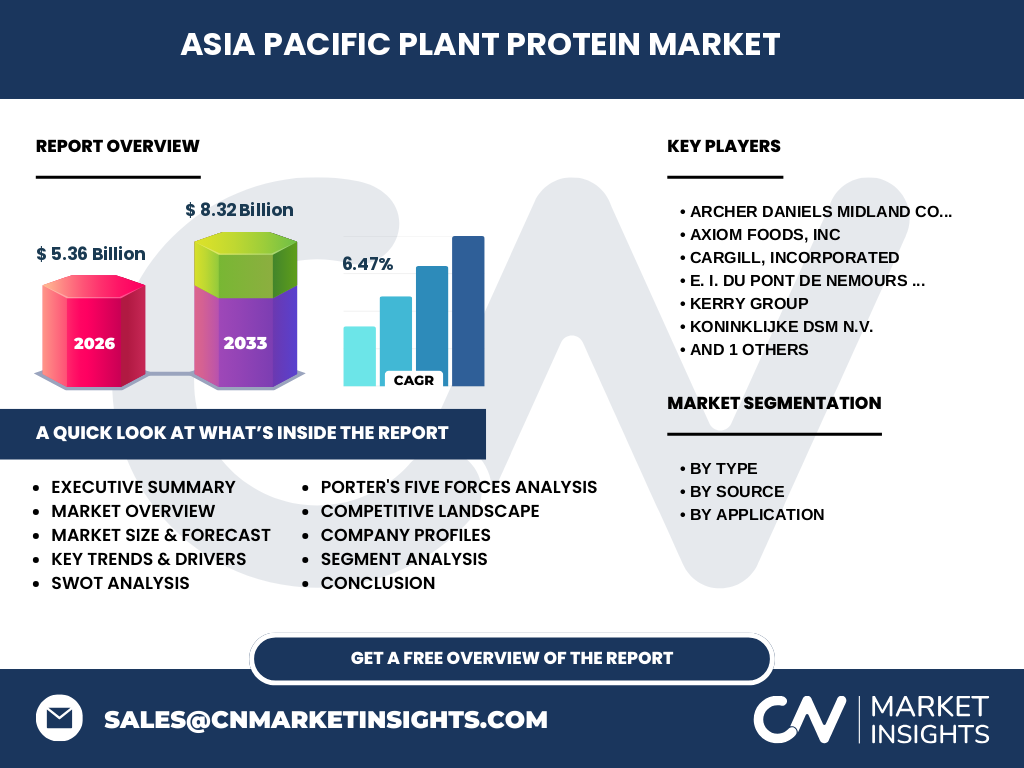

6. Executive Summary - High-level overview and key findings about Asia Pacific Plant Protein Market?

The Asia Pacific Plant Protein Market was valued at US$5.36 billion in 2026 and is projected to reach US$8.32 billion by 2033, reflecting a CAGR of 6.47 %. Growth is propelled by health and sustainability drivers, with soy, wheat, and pea proteins forming the core supply base. Isolates and concentrates lead the product mix, while applications in dairy alternatives and meat extenders account for the largest consumption. Competitive dynamics show consolidation around major agribusinesses and rapid innovation by specialty firms. The market outlook remains robust, with expanding middle‑class populations and supportive policy frameworks underpinning continued expansion.

7. Asia Pacific Plant Protein Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 6.47 %, the market is expected to maintain steady growth through 2032. By 2027, the market size will approach US$5.9 billion, climbing to US$7.0 billion by 2030, and reaching the forecasted US$8.32 billion by 2033. Growth will be evenly distributed across product types, with isolates experiencing the fastest compound increase due to premium positioning, while protein flour will grow at a slightly slower pace, reflecting its use in bulk food manufacturing.

8. Asia Pacific Plant Protein Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by type shows isolates commanding the highest value share, driven by demand for high‑purity ingredients in dairy‑free beverages. Concentrates hold a strong position in meat‑alternative formulations, while protein flour is predominant in bakery and snack applications. By source, soy remains the largest contributor owing to established processing infrastructure, followed by wheat and the fast‑growing pea segment, which benefits from allergen‑free positioning. Application‑wise, dairy alternatives capture the largest volume, with meat alternatives and protein bars showing the fastest growth rates as consumer willingness to experiment with new formats rises.

9. Global Asia Pacific Plant Protein Market Size and Share by Region - Geographic distribution?

Within the broader global plant‑protein landscape, the Asia Pacific region accounts for the majority share, reflecting its sizable population base and rapid urbanization. While exact regional percentages are not disclosed, the market’s absolute size of US$5.36 billion in 2026 positions the region as the primary growth engine, outpacing North America and Europe combined. Key sub‑regional contributors include China, Japan, South Korea, Australia, and emerging Southeast Asian economies.

10. Regional Analysis of the Asia Pacific Plant Protein Market - Detailed regional market performance?

China leads the market with extensive soy processing capacity and a burgeoning middle class seeking plant‑based dairy alternatives. Japan exhibits a strong demand for high‑protein functional drinks, favoring isolates. South Korea’s innovative snack sector drives growth in protein bars and bakery applications. Australia’s mature food‑service industry fuels demand for meat extenders, while Southeast Asian nations such as Indonesia and Thailand show rising consumption of fortified protein beverages, reflecting growing health awareness.

11. Leading Company Profiles in the Asia Pacific Plant Protein Market - Industry players and strategies?

Archer Daniels Midland Company leverages global sourcing to offer cost‑competitive soy isolates, focusing on supply‑chain reliability. Axiom Foods, Inc. specializes in pea‑protein isolate technology, pursuing partnerships with beverage brands to co‑develop clean‑label drinks. Cargill emphasizes integrated processing, from grain procurement to final protein flour, targeting large‑scale manufacturers. Du Pont De Nemours provides functional blends that combine protein with dietary fibers, catering to bakery sectors. Kerry Group pursues innovation in dairy‑free matrices, while DSM invests heavily in R&D for enzymatic processing to improve yield. Roquette Fr concentrates on niche applications such as high‑protein bakery mixes, employing custom formulation services.

12. Porter's Five Forces Analysis of the Asia Pacific Plant Protein Market - Competitive forces assessment?

Threat of new entrants is moderate; high capital requirements for processing facilities create barriers, yet niche pea‑protein startups can enter via contract manufacturing. Bargaining power of suppliers is moderate; while soy and wheat are abundant, quality‑grade raw material for isolates is limited, giving some leverage to agribusinesses. Bargaining power of buyers is high, as large food manufacturers can negotiate pricing and demand tailored specifications. Threat of substitutes is low to moderate; animal‑based proteins remain alternatives, but health and sustainability trends reduce their attractiveness. Industry rivalry is intense, with several global players competing on price, quality, and innovation, fostering continual product differentiation.

13. SWOT Analysis of the Asia Pacific Plant Protein Market - Strengths, weaknesses, opportunities, threats?

Strengths: Growing consumer demand, diversified raw material base, and strong backing from multinational agribusinesses. Weaknesses: Price sensitivity in emerging economies, reliance on a few key crops, and variable regulatory frameworks. Opportunities: Expansion into under‑penetrated markets, development of allergen‑free proteins, and partnerships for functional product creation. Threats: Crop supply disruptions due to climate change, potential trade restrictions, and competitive pressure from emerging alternative protein sources such as mycoprotein.

14. Asia Pacific Plant Protein Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with agricultural production of soy, wheat, and pea crops, followed by cleaning, milling, and extraction processes that generate isolates, concentrates, and flour. Mid‑stage activities include formulation, blending, and fortification to meet specific application requirements. Downstream, manufacturers integrate these ingredients into finished goods—beverages, dairy alternatives, meat analogues, bars, and bakery items—and distribute them via retail, food‑service, and e‑commerce channels. Key value‑adding steps are protein purification (isolates) and functional modification (solubility, emulsification) that differentiate premium products.

15. Key Investment Insights in the Asia Pacific Plant Protein Market - Strategic investment recommendations?

Investors should prioritize companies with vertically integrated operations that secure raw‑material supply and possess advanced purification technologies, as these assets mitigate cost volatility. Funding innovative pea‑protein firms can capture the fast‑growing allergen‑free segment. Strategic joint ventures with local food manufacturers enable market entry into high‑growth Southeast Asian countries. Additionally, allocating capital toward R&D for hybrid protein blends aligns with the flexitarian trend and offers higher-margin product opportunities.

16. Asia Pacific Plant Protein Market Conclusion - Summary and key takeaways?

The Asia Pacific Plant Protein Market is on a strong growth trajectory, valued at US$5.36 billion in 2026 and projected to reach US$8.32 billion by 2033 with a 6.47 % CAGR. Drivers such as health awareness, sustainability concerns, and rising incomes are robust, while challenges around raw‑material consistency and price sensitivity are manageable through innovation and supply‑chain diversification. Competitive dynamics favor firms that combine scale with specialized protein technologies. The outlook remains favorable, presenting compelling opportunities for manufacturers, investors, and policymakers.

17. Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, integrating primary interviews with industry executives, secondary data from company reports, trade publications, and government statistics. Quantitative forecasts were derived using time‑series analysis anchored on the provided market size (US$5.36 billion in 2026) and the stated CAGR of 6.47 %. Qualitative insights stem from trend analysis, competitive mapping, and value‑chain assessment to ensure a comprehensive market view.

18. Research Scope - Coverage and limitations?

The scope covers the plant‑protein market in the Asia Pacific region, focusing on isolates, concentrates, and protein flour derived from soy, wheat, and pea sources, and their applications across beverages, dairy alternatives, meat alternatives, protein bars, and bakery. The study excludes animal‑based proteins, non‑food industrial uses, and detailed country‑level financials beyond the aggregated regional figures provided.

19. Key Companies and Recent Developments in the Asia Pacific Plant Protein Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Archer Daniels Midland Company announced a new high‑yield soy‑isolate plant in China, targeting dairy‑free beverage manufacturers. Axiom Foods, Inc. launched a pea‑protein isolate line certified non‑GMO, partnering with a leading Southeast Asian beverage brand. Cargill introduced a blended wheat‑pea protein flour designed for bakery applications, emphasizing improved dough stability. Du Pont De Nemours released a functional protein‑fiber blend for meat‑alternative producers, highlighting clean‑label credentials. Kerry Group unveiled a ready‑to‑mix dairy‑alternative base incorporating soy and pea isolates. Koninklijke DSM N.V. secured a strategic partnership with an Australian food‑service chain to supply premium isolates for premium coffee‑shop menus. Roquette Fr. introduced a protein‑enriched bakery mix for gluten‑free products, expanding its presence in the health‑focused segment.